Putting Reality Back Into Virtual Reality Forecasts

Early Days and Overhype: Putting Reality Back Into

Virtual Reality Forecasts

The word hype is defined by Webster’s as “to promote or publicize extravagantly.” Yes, analysts have been criticized historically over even overhyping an emerging market. We at DWR understand this criticism firsthand.

We also understand a phrase, courtesy of Columbia Business School Professor Eli Noam: “People have the tendency to overestimate the impact of change in the near term, and underestimate it in the long term.”

This is why we are attempting to put some reality back into virtual reality (VR) forecasts.

It is helpful to put parameters around buckets of VR, as well as Augmented Reality (AR), and the likely very long-term winner bucket, meshed VR/AR. The challenge is both fun and challenging: Are the buckets defined by operating system? By hardware? Tethered or wireless? By operating system? Experience genre? Price? Frame rate?

From our perspective, the timeframe for rollout of VR and AR solutions helps support definition more than any technological specification. There are two big buckets in the near term, meaning the next 24 months: First, AR, and second, VR, sub-segmented by the low-end, middle-tier, and high-end markets.

Third, the discussion of 25+ months can be found later in this document. Fourth, there is a discussion of a critical, undercovered aspect: the marketplaces for content tied to hardware solutions.

Fifth, and final, the forecasts: DWR takes its best shot at estimating the size of the VR hardware markets over the next four years.

FIRST: Augmented Reality—Easy category…for now.

AR is fairly straight forward: check back in the 2H of 2017 to see if the needle on unit penetration has begun to rise yet. AR holds huge potential in a wide range of scenarios, from healthcare to communications to education to gaming to broader entertainment scenarios, but the lack of hardware and applications are the current status quo. These are early days of an ecosystem being built.

We have seen early examples, such as using a Microsoft HoloLens with Skype, or playing a future version of its tremendous IP, Minecraft, to joining folks from the NASA Jet Propulsion Lab to visit the surface of the planet Mars. They are compelling, but the computational analysis (think big math processing) to bring AR from an example to a viable, reasonably priced consumer, educational or business model will take time. The pure math behind AR requires computational analysis that can first, scan a room or space; second, calculate an overlay of the AR app into that room/space, and then re-run both of those calculations should the person wearing the AR device actually move, requiring a re-scan/adjustment and changes to the overlay. And, the transfer I/O speeds today favor a tethered solution vs. a wireless solution.

The good news is that Moore’s Law works in favor of AR. Compute technology will continue to increase at a rapid pace, storage costs will come down, transfer I/O speeds will increase, and final retail pricing will come down from the current level of $3,000 per unit. This also means that, as transfer I/O speeds improve, the options for AR hardware increase.

But, to be clear, the computational capabilities needed push AR out of 2016 and likely into the back half of 2017. While there are multiple AR efforts afoot, they are early days. For example, Microsoft only started in early Spring 2016 to ship AR dev kits (PCs capable of programming AR apps). These are truly early days for AR.

SECOND: VR—A moving category, meaning, it’s moving and changing.

Let’s be clear: Oculus started its Kickstarter project on August 1, 2012. That date is not even four years ago, and it was 2013/2014 before other camps emerged from HTC/Valve, Sony, and Google, with off-shoots from companies such Samsung (Gear VR, based on Oculus). Yes, Google launched Google Glass in February 2013 ($1,300/pair of glasses), and has backed off of that specific area, but Google Cardboard continues to dominate the low-end of the market.

In other words, there has been a mad rush of investment in this area in the past three years, with roughly six platforms, and that is not including any future entries. It is likely that heavyweight companies such as Apple (purchased Metaio, an AR company and has filed patents for VR with an iPhone) and Amazon will become involved because this category will be too big to ignore over time. Google is invested in Magic Leap, too, which is likely focused on the VR and/or meshed VR/AR market. Further, Asia/Pacific mobile titans such as Tencent, Alibaba, Giant Interactive, Softbank and NCSoft are likely looming. LG, too, will likely fast-follow the footsteps of Samsung with a significant phone-based entry effort.

As a result, we can look at the next 24 months, and then speculate with everyone else for 36 months and beyond. Again, we are in Early Days, and the long-term impact is likely significant.

So what are the near-term categories? Four make sense:

1.High-end PC, tethered

2.Low-end mobile phone, head-mounted devices (Phone HMD)

3.(Middle-ground) Console VR

4.All-in-one

head-mounted devices (A little further out…).

1. High-end PC, tethered

This means the Oculus Rift and HTC Vive, which means consumers have to spend at least $600 for the unit plus a $1,000-$2,000 PC capable of handling the high-end graphics, memory and I/O. This is the definition of a “high-end” experience to what DWR defines as a United States, mainstream audience: Joe Six-Pack in Middle America.

Joe Six-Pack is not buying a Vive or an Oculus. Joe Six-Pack this year is deciding if buying an Xbox One or Sony PlayStation 4 is the right call. Those two consoles launched in 2013 and have likely sold a combined 61 million units worldwide life-to-date. The price point on the consoles has come down to $299 (or even lower on short-term deals), and at this point in a typical hardware console cycle, Microsoft and Sony (and still Nintendo) are looking to last-generation console owners (PS3, Xbox 360, Nintendo Wii) to finally make the jump to upgrade to a “next-gen” Xbox One or PS4 console.

This is part-and-parcel with Joe Six-Pack having made the jump in the past three years to an HDTV, but have likely not bought in yet to a 4K TV. The Six-Pack family remains price sensitive and will look for discounts and bundles, but the bottom line is a high-end PC-based tethered VR experience is not on the 2016 Holiday Shopping List.

Will the Generation Me buyers rush to buy a high-end, tethered PC experience? Generation Me, also known as Gen M (18-to-30 years old), are social media champions, mobile device advocates, and are the reason for the future breakup of the current cable and satellite providers due to their a la carte behavior when it comes to media consumption. Gen M shows little interest in paying for subscriptions for music, TV and film and is more likely share passwords to streaming accounts.

They are mobile, meaning they use phones, tablets and laptops. They likely don’t own a high-end PC and see little value in purchasing one at this point. Would they buy an inexpensive, phone-based head-mounted device? Sure.

Or even better, they’re likely to use a Google Cardboard solution (as long as they didn’t buy the BIG Apple iPhone 6). It’s cheap and gets the Gen M’er into the experience. Perfect.

Alas, this demographic shrinks the total available market (TAM) for a high-end, tethered PC VR experience.

This is likely not new news to the management teams at Oculus and Rift. However, the splintering of the product for future products likely begins there. What that means is Valve, which is working with HTC on the Vive, understands the high-end PC gaming market better than any other company. They understand better what their TAM is and who their audience is, and may be perfectly content to serve what is a loyal, dedicated and paying high-end PC gamer market.

We also expect Valve to increase its number of partnerships to form other VR headset solutions. This may also include lower-priced VR solutions.

Oculus, however, was bought by the largest social media company on the planet, Facebook. While the goals of the two groups, Facebook and Oculus, remain independently focused, it is logical to expect that Facebook will want Oculus to grow bigger, wider, deeper, higher, and in any other dimension Facebook can imagine.

DWR has been engaged in voluminous discussions about “Why did Facebook buy Oculus?” with an inevitable response illuminated of “because Facebook wants social in VR!” We respectfully disagree. VR remains a tremendous long-term technology that has the capability of changing the landscape in many verticals. Facebook has a potentially dominant technology and future revenue stream in house, especially if Facebook should either face new competition or have a gradual decline due to numerous other quicker, more agile apps replacing single Facebook functions. Facebook’s biggest challenge is “death by a 1,000 cuts” as Gen M uses new apps to replace tools previously used on Facebook, one by one.

Oculus is critical to the long-term vision of Facebook as a whole and a nice additional potential revenue stream. This is a significant difference with respect to what HTC/Valve is doing with Vive.

This difference means that Facebook/Oculus has longer-term plans beyond being a high-end, tethered PC solution. That future likely involves moving the Rift technology a) down the value chain to lower-priced devices and b) non-tethered. But if you’re a groundbreaking technology company, you have to start somewhere. And Oculus started with a target market with $$$ – the high-end PC market, tethered.

2. Low-end, Phone HMDs

What we mean by low-end is the $99 and under, head-mounted display (HMD) units powered by a mobile phone. This means that the entry into VR means they have to own a mobile phone, and can attach it to a relatively cheap HMD. This is not a $700 solution requiring at least a $1,000 PC companion. This is a Google Cardboard or a Samsung Gear VR HMD, as well as the flood of knock-offs in this tier. (Do note that while a Gear could be $99, Cardboard is $15.)

This is a market that could appeal to Joe Six-Pack, as long as Joe Six-Pack has been updating his/her phone. Google Cardboard makes VR sampling, for a lack of a better term, viable. NY Times subscribers who have one can experience some of the short clips made available on the website. Samsung Gear VR owners have a chance to purchase content, such as games, entertainment or experiences, through the online store. Gear VR has an early, first-mover advantage by having the broadest early library of content available for consumers.

Gen M phone users will use Google Cardboard, and likely more than a Samsung Gear VR give the roughly $5 vs. $100 price points. Based on DWR research, Google Cardboard is a cool, fun, short-session experience. Short-session, in this case, is typically under five minutes. [This contrasts with longer, more intense experience with, for example, on an Oculus Rift. This experience can be 20 to 40 minutes, with occasional breaks.]

This low-end, phone HMD is the “fat” part of the market, meaning the largest number of early adopters of VR. It doesn’t mean they’re paying adopters (paying $60 for a game or experience), but they’re interested in the technology.

3. (Middle-ground) Console VR

This is an interesting market slice because of the business goals of the biggest two companies involved, Sony and Microsoft, with Nintendo remaining a wildcard heading into its 2017 console platform launch. This is called the middle ground from a pricing perspective – not as expensive as a high-end tethered PC solution and not as cheap as the low-end Google Cardboard.

Sony pushes entertainment through VR, led by gaming

Sony has a corporate goal of making the Sony entertainment brand, the PlayStation, a massive, global success. Sony as a corporate entity has suffered much of the past decade, shedding business units, reducing products, selling real estate, and laying off long-time employees. Sony has been forced to reconfigure its business from the analog era to the digital era, and leading that charge has been the PlayStation 4. It is imperative to Sony that the PS4 be a success to continue, plain and simple. And the PlayStation Virtual Reality (PSVR) is a critical effort to drive sales of more units and usage of the current PS4 install base.

As a result, Sony needs PSVR to be a marketing hit. It will position PSVR, which launches in October 2016, as the only dedicated VR solution on the market. And Sony is correct—it is.

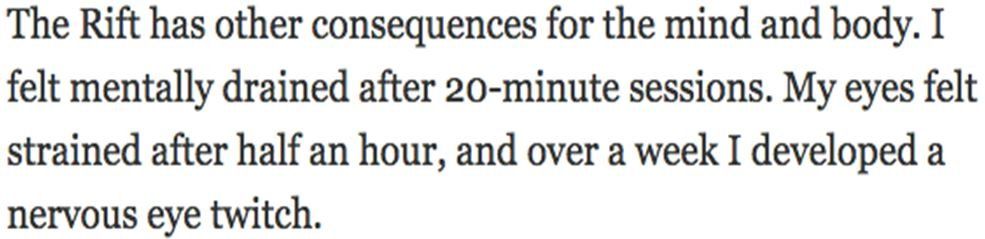

But, the one concern for Sony, and for every other VR solution on the market, is that it has to have to the best, non-nauseous experience on the market. Based on our research on DWR, short of heavily curating the content (games, experiences) flowing through the PSVR marketplace, Sony cannot prevent the likely consumer feedback/pushback that some VR experiences induce nausea. This is not an issue specific to Sony—it is a secular issue. We are in Early Days of this technology.

That said, we expect Sony to launch of limited range of experiences on PSVR this Fall. Sony should be given credit for pushing hard on VR, but must take steps to avoid reviews, for example, where the NY Times said:

So, expect or hope for Sony to learn from others: no “nervous eye twitch” inducing games. Again—Early Days.

The other subtle change Sony has made heading toward Holiday 2016 is broadening the PlayStation brand again back to entertainment, in lock-step with its November, 2016 launch of the PS4 Pro. Sony wants its brand to gain some of the shine the brand had in the 1990s and 2000s, when it stood to consumers meaning all things entertainment. Sony is currently running an ad campaign (including TV ads) for watching TV through Sony’s TV offering, PlayStation Vue. It is another prong for the PS4, in addition to the PSVR.

So what will

Microsoft do in VR?

Hello, Switzerland!

While we say that in jest, the reality is Microsoft sees the near-term jousting of low-end mobile HMD and high-end PC, tethered, and wants to stay above the fray while enabling multiple solutions in both VR and AR. We give Microsoft credit for not simply pushing all of its efforts behind Hololens and ignoring VR. The reality is their business strategy is not to be tied to just one VR or AR hardware solution, but to enable a variety of solutions.

Microsoft has already launched the Xbox One S console, which enables 4K streaming of video content and up-resolution for games. The next Xbox console, code named Project Scorpio, will have a full GPU and CPU upgrade which means it will support true 4K gaming when it launches (Holiday 2017).

So will Microsoft launch its own VR (or AR) solution? History suggests that Microsoft has sometimes launched its own hardware solutions (such as laptops or in the music space with the Zune or Windows Media Players, or even phones), but the corporate strategy has varied. Sometimes, Microsoft wants to seed a market. Other times, Microsoft has stepped up when partners have failed to spark or drive a market. Or, Microsoft has wanted to create a great solution to show its struggling partners a path to follow.

Microsoft created the Xbox hardware and several peripherals, such as multiple iterations of the controller, as well as the Kinect. Microsoft has learned, too, through successes and failures of when to cut bait or keep fishing. Our position is bifurcated—we would posit two points:

·Microsoft will likely create an AR hardware product, and while gaming will be a facet of AR, the application and promise for AR—as seen by Google but not fully delivered on with Google Glass—will be fulfilled in multiple, non-gaming verticals, such as enterprise and communications.

Microsoft will likely partner with others such as Valve to make a VR solution that worked on the Xbox One and was fed by apps from both the Xbox Live Marketplace and Valve’s Steam service. Conversely, Microsoft will likely become one of several Valve VR hardware partners.

While there has been discussion of “mesh” technologies that combine both VR and AR experiences into one hardware solution, we don’t believe this is viable as a mass market solution before 2020.

For more on the benefits of morphing the Xbox One into Windows 10-enabled console, see the DWR piece, see the DWR piece entitled Digital Empire Building: The Business Model Case for Windows 10 and VR on XBOX One.

Does Nintendo have a role in VR in the future?

Our working assumption is that Nintendo focuses more on great consumer experiences and less on what the latest technology feature to come on the market might be. Nintendo has pioneered VR in video gaming through the Virtual Boy in 1995. Yup, 21 years ago.

In 2008, the TV markets shifted to 3D TVs with required proprietary, bulky plastic glasses. The lack of standards for the glasses, as well as wearing the glasses themselves, stunted penetration of 3D TVs. However, Nintendo rolled out its own flavor of 3D gaming through its Nintendo 3DS in 2011—without requiring any additional glasses. Again, Nintendo put its own spin on 3D technologies and in its own time frame that remained focused on the consumer experience of fun in gaming.

4.

All-in-one HMDs—the new category

If you look at the two current market positions, $99 solutions or $2,000 solutions, this assumes that market dynamics will push forces two ways: the low-end up or the high-end down. Moore’s Law certainly backs this likelihood, complete, with price movements toward the middle of these two price points.

So this begs the question: Which price point moves to the middle fastest? This is likely solved by first answering the business model question: What business model exists in the middle ground? The razor/razor blade model will likely still be in effect, meaning companies will want to sell their hardware units at breakeven or a slight loss, while making up profits and margin on selling software/apps/games/entertainment solutions. This favors the low end in the near-term because of typical market dynamics.

This means that we could see standalone, or all-in-one HMDs, coming to the market in 2017. The technology is there for converting mobile phone technology into an HMD, and the price point is likely $499~$999, which places it in between Google Cardboard and an Oculus Rift.

In other words, in the middle of a wide middle ground.

The technology pieces needed for VR are morphing – Google is likely optimizing a version of its operating system with Daydream to help with I/O, battery life, and intense usage, and chipsets could be modified for the same types of upgrades. Then go a step further—take a mobile phone configuration and strip out all of the phone aspects to focus the chipset on a mobile VR experience, and this could be a scenario we see on the market in 2017. It likely wouldn’t be mass market volume due to manufacturing efficiencies and unit pricing until 2018-19, but it would drive, from a technological perspective, an all-in-one HMD solution.

DWR’s position is that this is more likely in 2017 (or sooner), with a company such as Magic Leap entering the fray in this category. Further, by the end of 2017, could Oculus have created a cost-reduced solution with a cheaper PC to get the total solution below $1,000? Maybe, but Moore’s Law, again, suggests that this scenario is more likely 2018, short of Oculus launching an all-in-one HMD that doesn’t match up to current high-end PC specifications. This latter scenario would suggest an all-in-one HMD for Oculus in 2017 and possibly more accurately reflect corporate goals of market penetration for versions of the Rift.

THIRD: So what happens in 25+ months?

The rise of the New Entrants

One of the most likely disruptions to the VR market, beyond all-in-one HMDs, will be the rise of the new entrants. We believe there are a few, big companies out there who could enter the VR market: Tencent, Apple and Amazon. Here is the case for each of them:

·Companies new to VR enter the market in 2017/2018, but not new companies: Tencent, Amazon and Apple. Adding VR and/or AR is a reasonable building block for Digital Empire Building for big (and getting bigger) players in the consumer space, hence:

oTencent has slowly been building multiple pieces of

the food chain for VR from content to engines to mobile gaming, and likely have

manufacturing partnerships lined up in China. Tencent has three major

subsidiaries, Riot Games, Epic Games, and Supercel, as well as social layers

such as QQ Chat.

With the evolution of e-gaming, led by Riot, the next logical step beyond

filling The Staples Center for a tournament is to have it available for a small

price via VR for all the fans who could not travel to Los Angeles. This is part

of a larger entertainment expansion via VR, but easily crosses over to

e-gaming.

oAmazon, too, has been building multiple pieces

from Lumberyard to content acquisitions, with payment systems, etc., already

in-house. Amazon already has users, payment systems, games through FireTV, and

infinite amounts of data on consumers. We could envision a headset that works

in part with a future Kindle Fire TV and its apps universe. It would likely

move beyond just games, too, just as it has diversified its video content as

well.

One potential source for VR entertainment will be Amazon’s strategic

acquisition: Twitch. Gamers today can subscribe to watch Twitch for following

gaming experts, and subscribe and follow them on YouTube, too. Now, instead of

watching a stream via Twitch, why not watch it in VR? We think this is a

logical next step, especially given that VR capture cameras will rapidly come

down in price over the next 24 months.

oApple. Of course. Will be a feature for an Apple

iPhone? If we had to guess, we’d say no—rather a standalone hardware device

tied to the App Store and Apple TV. We find it hard to see Apple not wanting to

have a presence in this market, especially given Apple can waterfall VR

hardware in typical Apple style—starting with a fully-priced high-end product.

The contra argument for Apple bears merit, in that Apple has the App Store,

featuring content that makes either Apple’s operating system or hardware look

fantastic—the best experience for consumers, best photos, best way to consume

music, etc. The App Store is built to drive highly profitable hardware margins,

north of 30%. So, if Apple goes down the VR route, it would likely need the VR

hardware to be high margin, fed by the App Store, which could happen through

Apple TV.

Looking to 25+ months from now is the part of any crystal ball is typically the most foggy. The working DWR assumptions include that in 25+ months…

·Microsoft will have partnered with a company such

as Valve for a VR solution for Xbox One, featuring both the Xbox Live and Steam

marketplaces.

·Microsoft will have rolled out a high-end, v 1.0 AR solution.

·Sony will be bundling a price-reduced PS4 Pro with the PSVR.

·Oculus will have a mid-tier priced PC solution.

·Oculus will have partnered with non-gaming and

entertainment partners in verticals such as health care, science, education and

communications.

·Both Oculus and Valve will have partnered with more hardware manufacturers for both high-end and eventually, mid-tier (priced) solutions.

·Google Daydream

likely holds the largest market

share because it gains rapid adoption given the massive global install base of

Android-based phones.

·Samsung

continues to promote Samsung Gear VR as a peripheral to its Galaxy phones, and eventually

creates its own Milk Music-equivalent

for VR apps in conjunction with the

Powered-By-Oculus Gear VR marketplace today.

In 25+ months, we expect to see VR experiences

and games redefined.

Right now, many developers are becoming comfortable with the features and capabilities of VR (i.e. getting scared by a shark while diving, vertigo-inducing cliff walking), but a truly, bottoms-up new transformed experience should arrive in 25+ months, hopefully sooner. Entertainment needs to be created in VR, not just ported over from a console or PC game, or having just a portion of a game be VR-enabled.

Today, gamers are used to either short-session mobile games, or long-session console games. Early on, VR will be more likely short-session games, but in 25+ months, we would expect to see the beginnings of long-session VR games.

FOURTH: One other key piece for VR – the marketplaces

The basic parts for VR include hardware, an operating system, and software/apps to drive adoption and usage. So what do VR marketplaces look like today? Fragmented.

A key question is “How does a consumer connect to a store, and which store?” There are currently islands:

·The Samsung Gear VR, powered by Oculus, works with the Samsung Gear.

·The Oculus Rift works with a slimmed down version of the Gear VR store, as well as with select Steam content.

·The Vive works with Steam.

·The Hololens will likely work with the Xbox Live Store, as well as other Windows 10-based stores.

·Google Cardboard works the Google Play Store.

·The Sony PSVR will work with the Sony Playstation Store.

That means there are six, mostly not-interoperable markets, which are signs of early days and fragmented markets, driven by competing operating standards and corporate goals. This is not helpful with driving consumer adoption and, rather, promotes consumer confusion. This is also typical of early days as consumer adoption can be stunted by confusion until a few big winners emerge and others fall off. We are 25+ months away from that shakeout beginning to happen, and the winners will have integrated, easy-to-use online stores or marketplaces to find a range of content.

What we are looking for is integrated markets – where a Valve-based VR device, connected to an Xbox One and running on Windows 10, can provide an easy experience for a consumer to access content from Steam or the Xbox Live Marketplace. This is a win-win; consumers win, and both Valve and Microsoft win. Microsoft has already gone down the route of launching its Xbox Play Anywhere campaign, and critical to that success is having a unified store for both Xbox One and Windows 10 gamer.

Fifth: The VR Hardware Forecast

Yes, this is what is called, “burying the lead.” However, this is not a simple subject and not a simple forecast, so the logic behind how markets could emerge is detailed in the prior pages. Additional color for parts to the forecast are included below.

This forecast was put together from a combination of discussions with industry participants this year. Segmenting the VR universe has been complex because the tiers that exist today will morph in the next three years, and not only will current participants in tiers likely move up or down with new products, but there will also be new entrants not yet directly involved in VR, but involved in other gaming segments in mobile, console or PC.

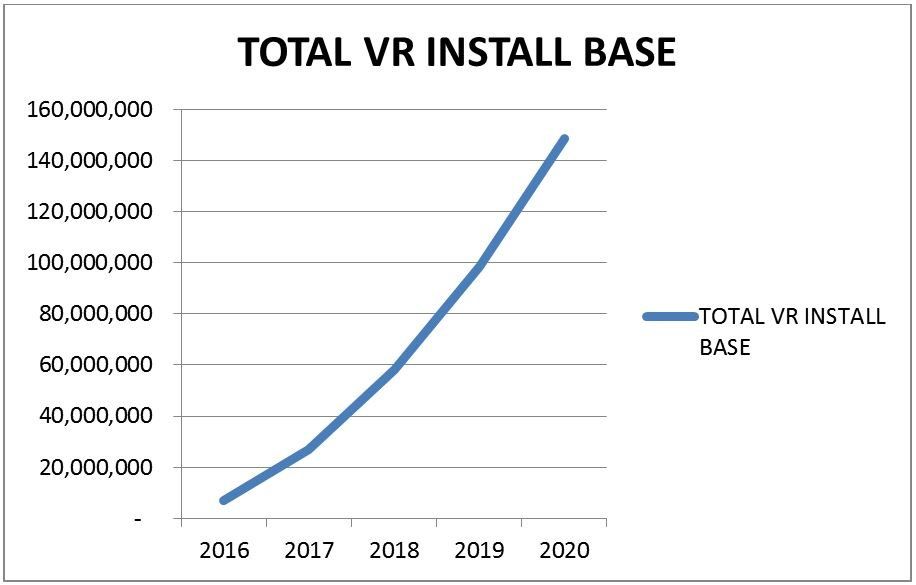

The total VR install base, based on low-end VR products, middle-ground console VR, and high-end tethered PC VR, is forecast to be at 8 million units in 2016, heading toward 150 million in 2020. Note that Google Cardboard is not included in this forecast, as we consider it a VR sampler, or introduction into VR at this time. We also believe that the new entrants, such as Tencent, Apple and Amazon, could add another 30 million units to this overall forecast in multiple tiers by 2020 — that 30 million unit number is not included in this forecast, but that forecast is available upon request to DWR.Graph 1: Total VR Install base, 2016-2020

Source: Digital World Research, 2016

We are forecasting this growth because we foresee solid growth through consoles, the advance of VR with mobile phones, and lower prices at the high end in the next three years thanks to Moore’s Law. We also expect a standalone VR hardware market to emerge thanks to adjustments to both mobile operating systems, increased mobile battery power, chipsets optimized for VR, and the emergence of a few compelling VR market places. One of the single biggest drivers behind our forecasts, too, is the emergence of a killer VR app: a built-from-scratch experience that reimagines VR entertainment. We assume this new app(s) will come in 2018, helping drive adoption and generating additional consumer interest while a variety of price points emerge for consumers to adopt a VR platform.

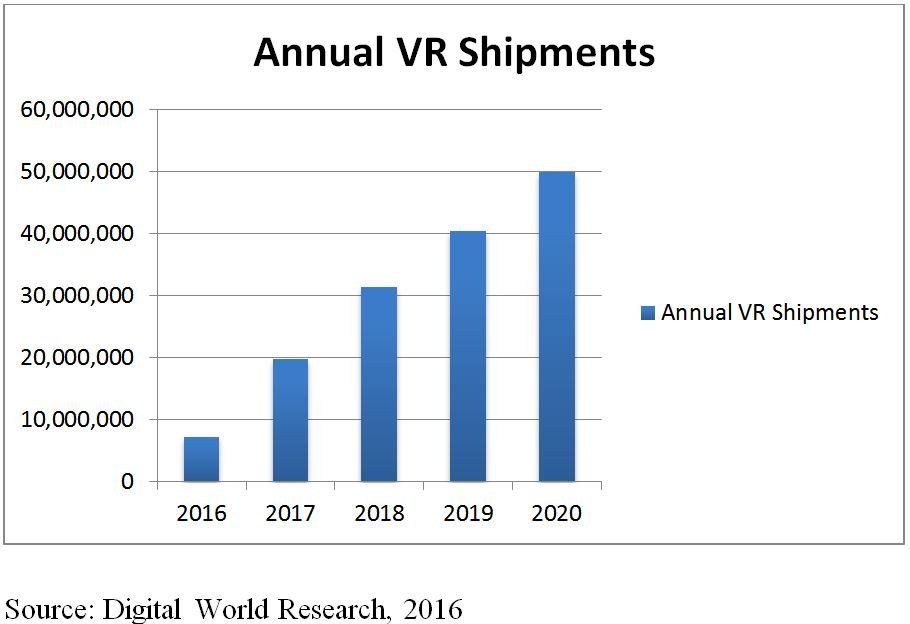

The annual VR shipments this year will be mostly driven by the low-end, highlighted by Samsung Gear VR, with Google’s Daydream platform having a big impact behind the forecast starting in 2017. We are forecasting just over 7 million units shipped in 2016, growing to nearly 50 million units shipped in 2020.

Table 1: Annual VR Shipments, 2016-202

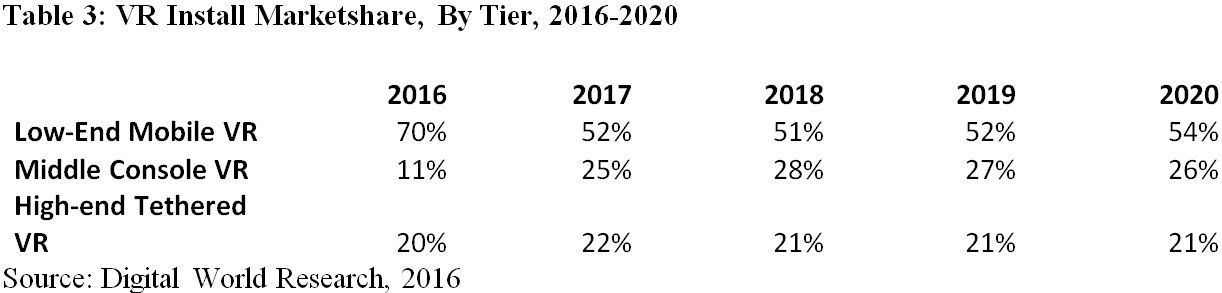

Table 2: Annual VR Shipments, by Tier, 2016-2020

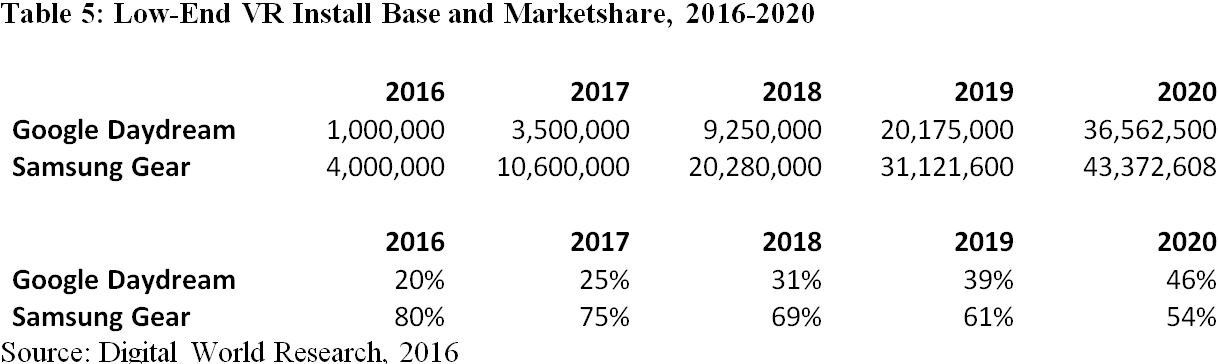

By tier, we expect the low-end segment to account for the largest percentage of the VR install base in 2016 at 70%, and ticking down to 54% over the next four years as the middle-ground console VR space gains traction.

Low-End

Mobile VR Tier—A Deeper Dive

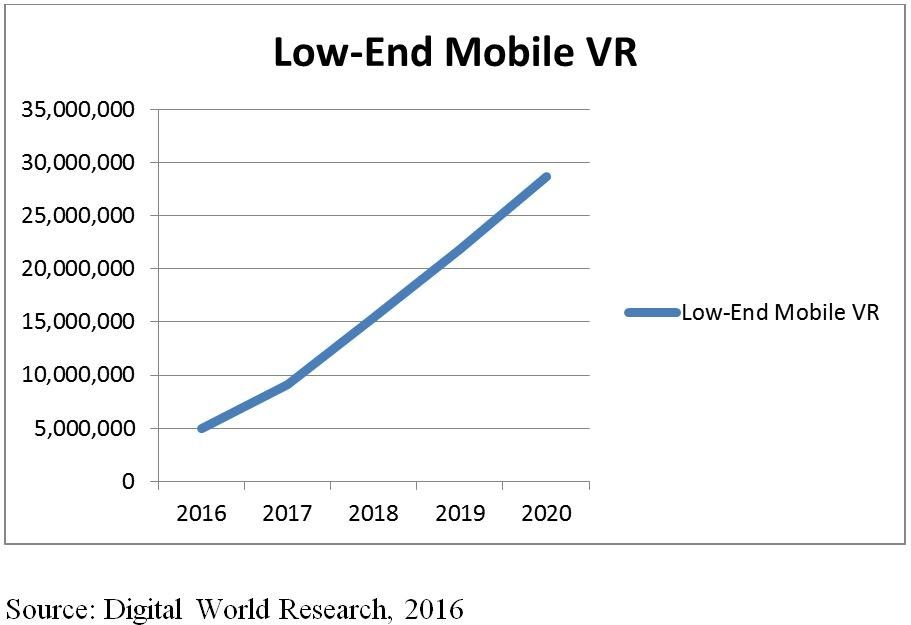

When looking more closely at the low-end VR tier, this is going to be the biggest path to consumer education and experiences around VR. We are forecasting 5 million VR units shipped in 2016, increasing to 30 million in 2020.

We are forecasting numbers based on the impact on two likely leaders, Samsung and Google. This forecast does not include a meaningful impact from LG, and the Google Daydream forecasted numbers could prove conservative. Further, a wildcard to this market is Asia-Pacific, led by China, because there are already easily 75+ knock-off low-end mobile headset manufacturers, but they will still need a phone and a marketplace to drive what we consider to be meaningful VR shipment growth. One forecast that is now being worked on is next tying hardware to app purchase and usage, driving the overall VR market in multiple verticals, in which China’s adoption rate of all VR low-end mobile devices may prove more important in our view.

Graph 2: Low-End Mobile VR Shipments, 2016-2020

It is our position that Google Daydream is going to be a significant product for Google and a bigger “hit” than Google Glass. After talking with multiple developers, the excitement around Daydream is high, and we are forecasting a ramp that may prove conservative. Again, we are forecasting for a baseline with upside.

Middle-Ground Console VR Tier—A Deeper Dive

The middle-ground console VR tier will likely be a significant avenue for consumers to play in VR. We forecast under 1 million units in 2016 (they start shipping in October) and could reach up to 12 million units in 2020. This forecast does not include any meaningful VR units for Nintendo with the NX at this time (see the Second section above for more).

If Sony has an install base of roughly 25 million PSVR units in 2020, and Microsoft has an install base of nearly 15 million VR units, this could mean roughly a tie ratio of 24%~31% to our forecast for all PS4 consoles and XBOX One consoles by 2020. We believe these are reasonable ratios.

In forecasting tie ratios, it is important to note that come 2017, Sony will have the original PS4 install base, the PS4 “slim” install base, and a new PS4 Pro install base. The performance of PSVR will be optimal on the PS4 Pro, but still possible on earlier PS4 consoles. This also means that the tie ratio for PS4 Pro owners will likely be higher with PSVR than PS4 original console owners. Part of the value proposition of buying a PS4 Pro is for full HD gaming and full HD streaming (Netflix, etc.), and owners of 4K TVs being enabled for a great experience.

It is possible, too, that either/or/both Sony and Microsoft could bundle in VR solutions with console shipments in 2018~2020, which would tick our numbers up.

For the XBOX One forecast, there is a similar challenge – the XBOX One, the XBOX One S, and next year’s launch of the XBOX One Project Scorpio. While the S current supports HD streaming, the holiday 2017 launch of Project Scorpio will enable full HD gaming and full HD streaming, similar to the PS4 Pro.

The other enabling technology advantage for Microsoft is running full Windows 10 on the XBOX One Project Scorpio, which means any PC-enabled VR solution, such as the Valve-HTC Vive or Facebook’s Oculus, could theoretically run on an XBOX One. This means the potential partners for VR for Microsoft are broad and why we have forecasted an inflection point in units for this tier in 2018.

Our breakdown forecast of PS4s and XBOX Ones, and tie ratios by console tiers, can be supplied upon inquiry to DWR.Graph 3: Middle-Tier Console VR Shipments, 2016-2020

We forecast a 5% tie ratio for PSVR early in this adoption cycle, and could prove conservative if Sony can ramp manufacturing in 2017 beyond our numbers. We also forecast Sony to continue its significant lead, nearly 2x, of the PS4 install base over the XBOX One install base.

The table below shows Sony’s forecasted marketshare lead in console VR, which is reflective of its continued dominance in this hardware cycle.

High-end

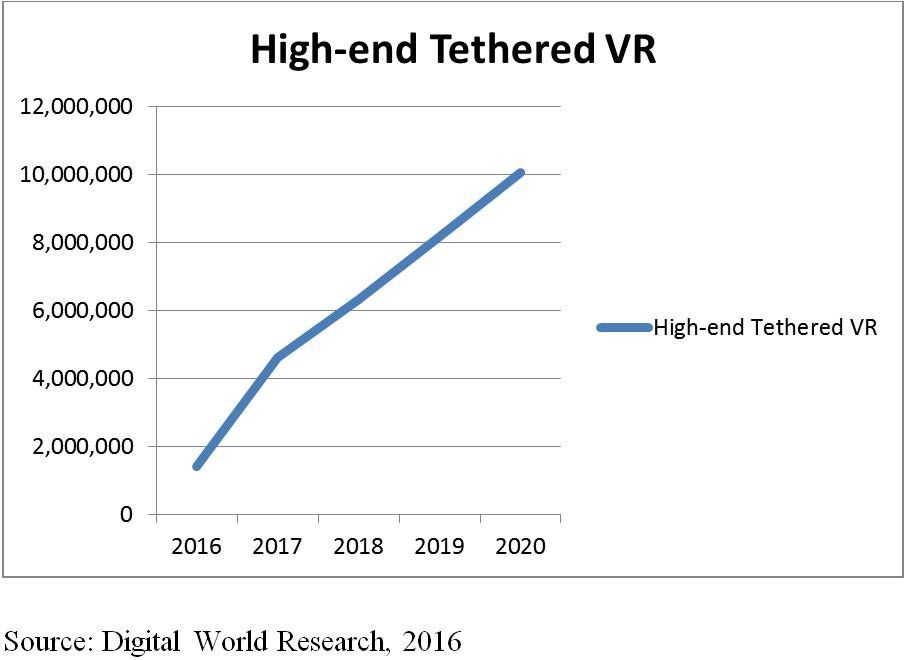

Tethered VR Tier—A Deeper Dive

The high-end tethered VR market is the driver of early excitement in this market, with Facebook spending $2 billion on acquiring Oculus and starting a modern-day Gold Rush with VC investors backing multiple VR efforts. While the segment has grown rapidly in the past four years, the high-end, while expensive with $1,500-PCs and ~$799 VR setups, have had some early success as manufacturing has ramped.

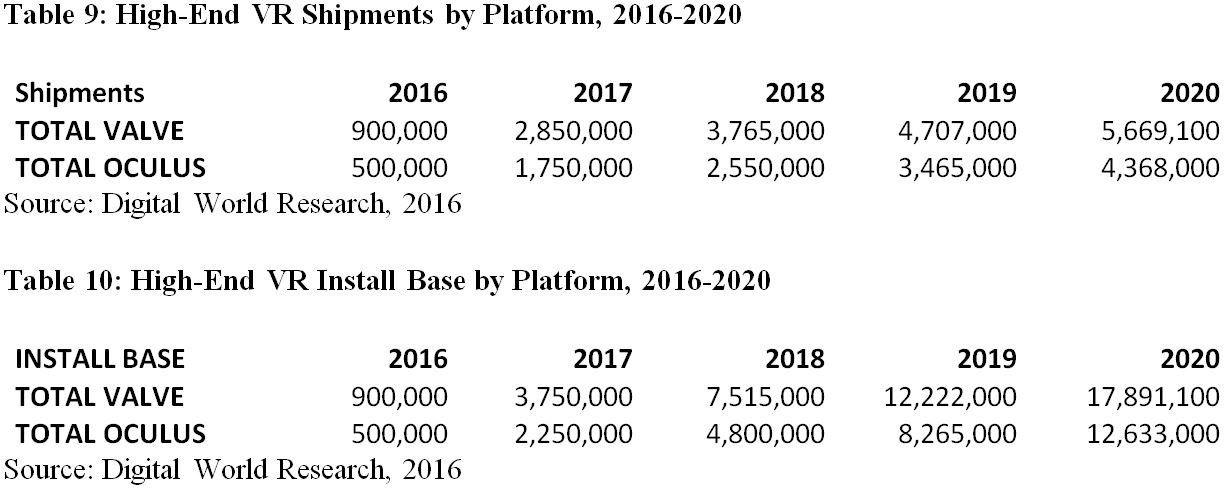

We forecast nearly 1.5 million high-end VR shipments in 2016, rising to 10 million units in 2020, driven by Valve and Oculus. We forecast an install base for high-end VR at nearly 30 million units in 2020.

The two main variables for growth in this tier are pricing and partners. Oculus has already cut its price on the Rift headset, and the faster the units can be price-reduced through volume manufacturing (and Moore’s Law), the faster the high-end VR tier can help morph into middle-tier units in the next four years.

While Valve has partnered with HTC for the Vive VR headset, we believe Valve will be aggressive with adding additional hardware partners and help fuel usage of its online marketplace (app store), Steam. Note that Steam is not simply an online marketplace, but it is a VR-friendly location to find new content that works with both the Vive and the Oculus Rift.

Graph 4: High-End Tethered VR Annual Shipments, 2016-2020

Depending on how rapidly Valve adds partners, and adds a mid-tier priced solution, could mean this forecast is conservative. Also note that we forecast an inflection around the launch of the XBOX One Project Scorpio box as well.

The other factor for VR adoption, especially in the case of Oculus, will be the expansion of VR beyond gaming and entertainment. Longer term, while Valve is focused on gaming, Oculus remains focused on multiple verticals beyond gaming such as health care, education and communications. If a non-gaming vertical should gain significant momentum before 2020, the Oculus forecast could prove conservative.

The excel model for these forecasts is available upon request to DWR. >> Download the Printable PDF Here